How to Print Money with FRAX

The Ultimate Guide to Stablecoins, Part 1: FRAX, FXS, FPI, and FPIS

Stablecoins play a critical role in the cryptoeconomy, embodying the security guarantees of decentralized finance while also providing the price stability of more traditional financial assets such as fiat currency. This series details the mechanisms that power stablecoins.

FRAX Finance

Recently, FRAX has become one of the most popular stablecoins in circulation, with its supply increasing over 25,000% from $10 million to $2.6 billion over the past 6 months. Pegged to the U.S. Dollar, FRAX is notable for its innovative use of its native governance token as a form of collateralization. The key aspect that makes FRAX work is that market participants are incentivized to keep the price as close to $1 as posible.

Collateral

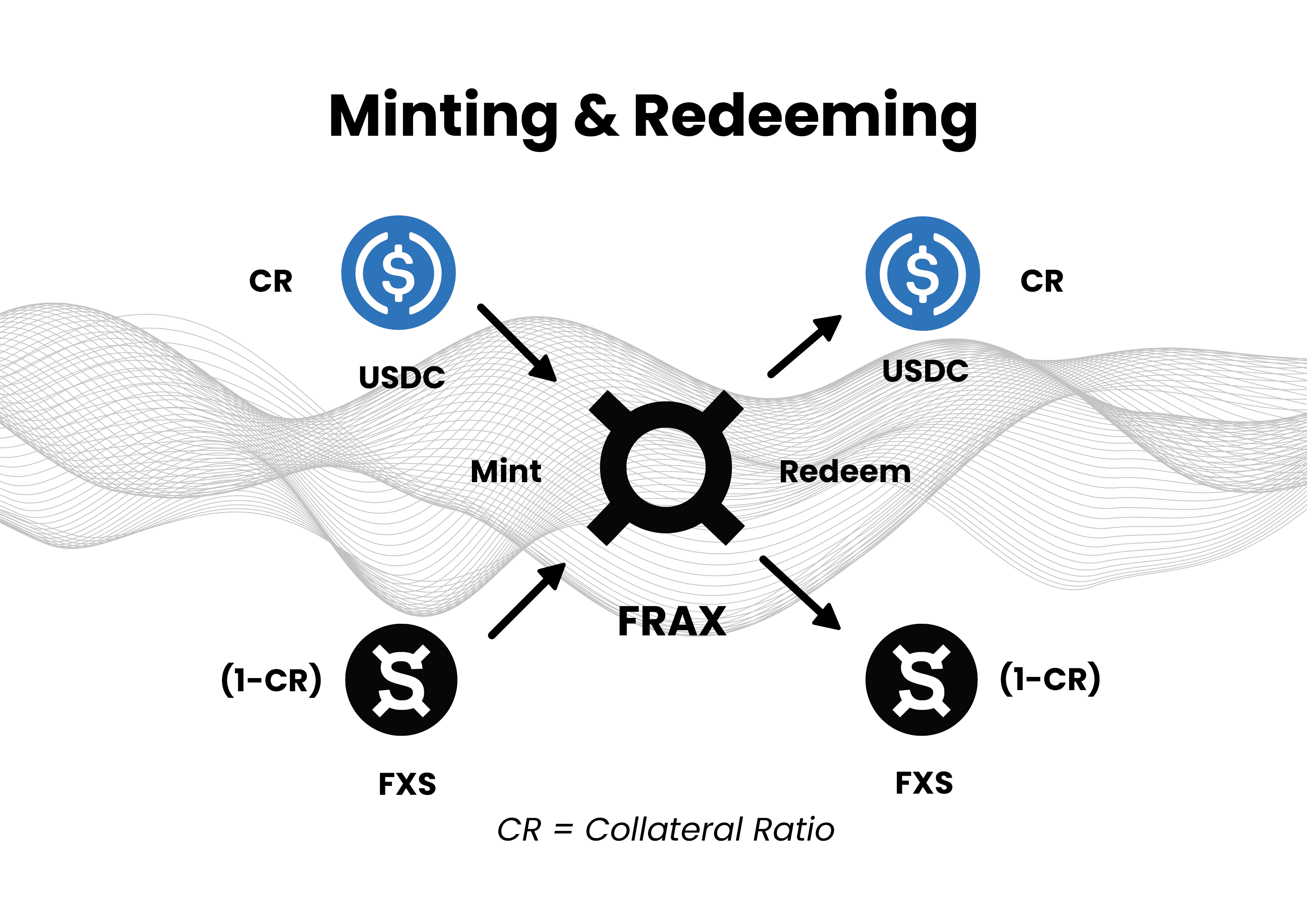

FRAX is a collateralized protocol. This means that FRAX is backed by other assets of value, and in order to mint FRAX, you must deposit those other assets of value. Conversely, you can also redeem these collateral assets by submitting FRAX. 1 FRAX can be redeemed for every $1 worth of collateral submitted, and vice versa.

The collateral submitted must be a mix of the following:

X% of it must be another stablecoin. The current list includes USDC, DAI, FEI, LUSD, sUSD, USDP, and USDC.

The number X% is known as the Collateralization Ratio.

(100 - X)% of it must be the protocol’s native governance token, FXS.

As an example, let’s suppose you want to mint 1,000 FRAX and that the collateralization ratio is currently 84%. You could do so by:

Acquiring 84% * $1,000 = $840 worth of USDC. Given that USDC is pegged to the dollar, this would be equal to 840 USDC.

Acquiring 16% * $1,000 = $160 worth of FXS. Given that FXS is currently trading at $21, this would be equal to $160 / $21 = 7.62 FXS.

Deposit 840 USDC and 7.62 FXS into the protocol, and get 1,000 FRAX in return.

The redemption process of submitting FRAX to receive collateral + FXS in return works in the expected way as well. For each of these processes, the user must pay a small fee in the range of 0.20% to 0.45% of the amount minted/redeemed.

There are several questions that naturally arise from the above mechanism:

What ensures that FRAX remains pegged to $1?

What determines the collateralization ratio?

Why does FXS have value?

We examine each of these in turn.

Price Stability

FRAX maintains its peg to the US dollar through the arbitrage of market participants. The protocol is designed so that the everyone is incentivized to make the value of FRAX as close to $1 as possible.

Suppose that FRAX were trading at $1.01 on a DEX like Uniswap. Then a market participant could make free money through the following steps:

Provide $1 worth of collateral and FXS, and mint FRAX.

Sell that FRAX for $1.01 on Uniswap.

Since the participant spent $1 and received $1.01, they made a 1 cent profit (ignoring fees and gas). If FRAX were trading at $0.99, then the inverse process (redemption) would also yield a 1 cent profit.

Minting and redemptions are actually disabled if the price of FRAX is relatively close to $1 (in the range $0.9933 and $1.00.33). In these cases, FRAX provides the “Buyback & Collateralization” mechanism to facilitate this price stability.

For the system to be at equilibrium, the amount of collateral in the treasury should correspond exactly to X * F, where X is the collateralization ratio and F is the amount of FRAX in circulation. However, this will not always hold, due to several factors:

The price of FXS changes

The collateralization ratio changes

The treasury accumulates excess collateral through fees

If the system is not in equilibrium, then the price of FRAX can fluctuate. In these scenarios where the actual collateralization is out of sync with the desired ratio, FRAX provides incentives for users to take action that will correct this imbalance:

When the actual amount of collateral is lower than the collateralization ratio, users can submit collateral and receive FXS at a 0.20% bonus. This is known as recollateralization.

When the actual amount of collateral is higher than the collateralization ratio, users can submit FXS and receive collateral in return. FXS is burned. This is known as a buyback.

Note the asymmetry: recollateralization is explicitly incentivized through a bonus, whereas buybacks are not. This is because the protocol being undercollateralized is a bigger risk to the system than being overcollateralized.

Through the combination of minting, redemptions, buybacks, and recollateralizations, arbitrageurs on the market ensure that the FRAX maintains its peg to the dollar because it is in their interest to do so.

Collateralization Ratio

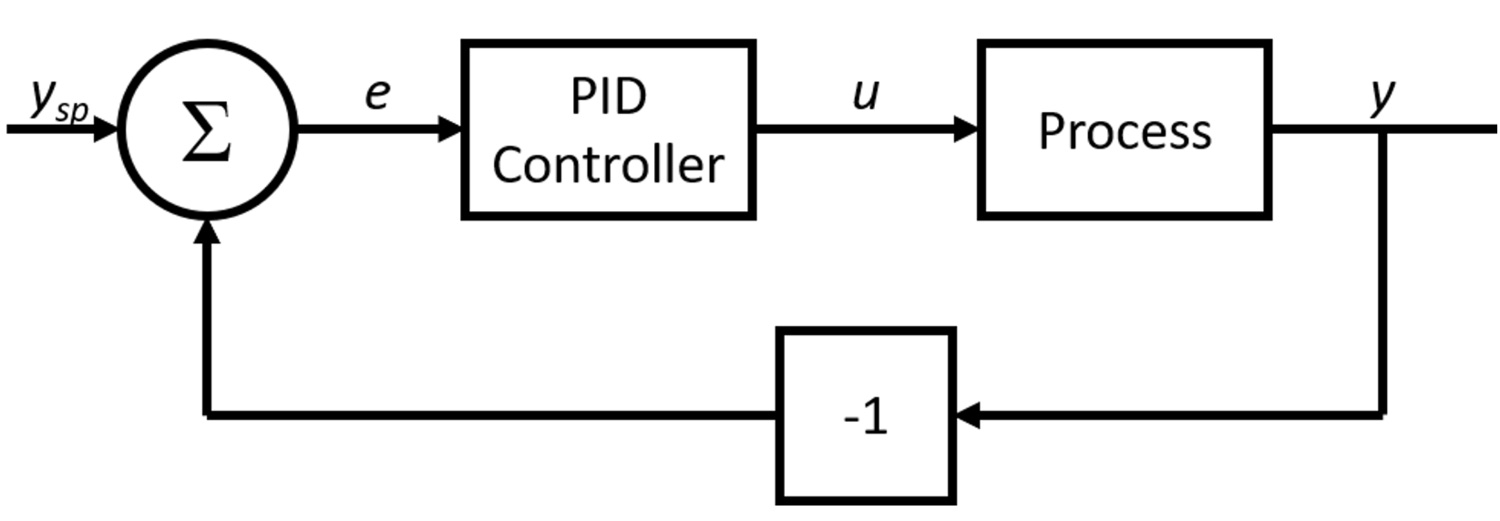

The collateralization ratio is set using an algorithm known as a Proportional-Integral-Derivative (PID) Controller.

PID Controllers are useful when a stable value needs to be achieved in an unstable setting. One common example is ensuring that a room remains at a certain temperature. Other variables that could be subject to a PID controller include air pressure and water flow.

A PID Controller takes the current value of the system (the Process Variable) and compares it to the desired value (the Setpoint), computing the difference between the two (the Error, denoted by the function e(t)). At each step, the PID controller outputs a value by which to change the current value, using three terms:

The Proportional Term - the Error, multiplied by some constant

The Integral Term - the cumulative Error up until now, multiplied by some constant

The Derivative Term - the rate by which the Error is changing, multiplied by some constant

The intuition behind the PID controller is that the Process Variable should be gradually nudged in the right direction by factoring in the current Error (the Proportional Term), the historical Error (the Integral Term), and the future Error (the Derivative Term).

FRAX’s PID Controller uses a figure known as the “Growth Ratio”, denoted G_r, as the Process Variable:

Fundamentally, the Growth Ratio measures how much FXS is in circulation relative to the amount of FRAX in circulation. If the Growth Ratio increases, then it means that excess FXS is in circulation relative to the amount of FRAX in circulation; thus, the collateralization ratio should be decreased so that the excess FXS can be burned. Conversely, if the Growth Ratio decreases, it means that less FXS is in circulation; thus, to output more FXS into the system, the collateralization ratio increases.

The PIDController is an ingenious application of an engineering construct generally reserved for the physical world. By perturbing the Collateralization Ratio gradually according to the Growth Ratio, the system ensures that the Collateralization Ratio is set to incentivize arbitrageurs to maintain the FRAX peg of $1.00.

FXS

What gives FXS value? By this point, you probably have some good guesses, and you would be right:

FXS is needed to mint FRAX.

FXS can be submitted for buybacks.

Fees generated from minting, redemption, buybacks, and recollateralization accrue to the Treasury, which is governed by FXS holders.

FXS can be vote-escrowed - users can exchange their FXS for veFXS. This gives holders the power to vote on governance proposals, including FRAX gauges, which determine FXS reward emissions on various pools.

This design is identical to Curve, CRV, and veCRV - for more on this, see this post.

Lastly, FXS holders were eligible for an airdrop of a new token called FPI, the Frax Price Index, on February 20, 2022. According to the documentation:

The Frax Price Index is a brand new, unique protocol within the Frax ecosystem. Centered around its own native stablecoin (FPI) and governance token (FPIS), the system will adjust every month according to an on-chain Consumer Price Index oracle so that holders of the FPI will increase their dollar-denominated value each month according to the reported CPI increase. It does this by earning yield on the underlying FPI treasury, created from users minting and redeeming FPI with FRAX.

The Frax Price Index Share (FPIS) token is the governance token of the system, which is also entitled to seigniorage from the protocol. Excess yield will be directed from the treasury to FPIS holders, similar to the FXS structure. During times in which the FPI treasury does not create enough yield to maintain the increased backing per FPI due to inflation, new FPIS may be minted and sold to increase the treasury. Since the protocol is launched from within the Frax ecosystem, the FPIS token will also direct a variable part of its revenue to FXS holders.

Analysis

The addition of an inflation-hedging asset in the FRAX ecosystem is certainly an astute one, given the current climate. American inflation is at its highest in 40 years and one of the most important political issues. People are looking for ways to preserve their hard-earned money, but the options are few: bonds do not outpace inflation; stocks are exposed to the risk of recession; and in the short term, Bitcoin is too volatile to be an inflation hedge. Thus, introducing a token that claims to track with inflation could be attractive to investors.

Nevertheless, the mechanism for funding FPI seems flawed: “during times in which the FPI treasury does not create enough yield to maintain the increased backing per FPI due to inflation, new FPIS may be minted and sold to increase the treasury.” In other words, FRAX proposes to create an asset that keeps up with US Dollar inflation, FPI, through the inflation of a different asset, FPIS. Printing money is printing money, regardless of whether the perpetrator is the Federal Reserve or a DeFi protocol.

Details on the FPI are yet slim, so we may see more color in the coming weeks and months that could legitimize it further.

Conclusion

FRAX deploys an array of clever techniques to ensure its value is close to $1 as possible. It allows arbitrageurs to deposit and withdraw collateral through minting, redemptions, recollateralizations, and buybacks, which then allows them to make a profit for maintaining price stability. The native governance token, FXS, is part of the collateralization, and its proportion of the collateral is dictated by the Collateralization Ratio. The Collateralization Ratio is nudged up and down through a PID Controller, a common construct in industrial engineering. FXS also allows for vote-escrow-based governance, similar to CRV. While the newly airdropped token FPI is theoretically enticing for being e pegged to the inflation of the US Dollar, it is unclear how FRAX will achieve this if the increase in value of the FPI is funded by inflation in another token, FPIS.

Subscribe & Share

Any views expressed on Incentivized are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.

another stellar article. the maths behind PID always seemed unapproachable to me til now. thanks!

I heard of FRAX for a while, but have been reluctant to dive into it (just like Kai). Now I am more confident to revisit the whitepaper and keep learning more. My appreciation for Yuga's BUIDLing!